TSP Withdrawal Options Explained: Lump Sum, Installments, or Annuity — What to Choose

You've spent 20 or 30 years contributing to your Thrift Savings Plan. Now retirement is here, and TSP is asking how you'd like to receive your money. The answer you give will shape your tax bills, your cash flow, and your financial flexibility for the rest of your life.

There is no universally right answer — but there are common mistakes. Here's what each option actually means, who it suits, and what to watch out for.

The Four Ways to Take TSP Money

TSP offers four distinct withdrawal approaches at separation or retirement. You can also combine them.

1. Single Lump Sum Withdrawal

You request all or part of your TSP balance in one payment. The money lands in your bank account (or rolls to another account), and TSP is done.

Tax treatment: The entire amount is counted as ordinary income in the year you receive it. Traditional TSP contributions were pre-tax, so you've never paid income tax on them — until now.

Flexibility: High, before you take it. Once it's gone, it's gone. You can do whatever you want with the cash — pay off a mortgage, fund a business, gift to family — but the tax hit is immediate and unavoidable.

Who it suits: Someone with a specific, large one-time use for the funds — paying off a mortgage being the classic example — or someone rolling the entire balance to an IRA. It is not suited as a primary income strategy for most retirees.

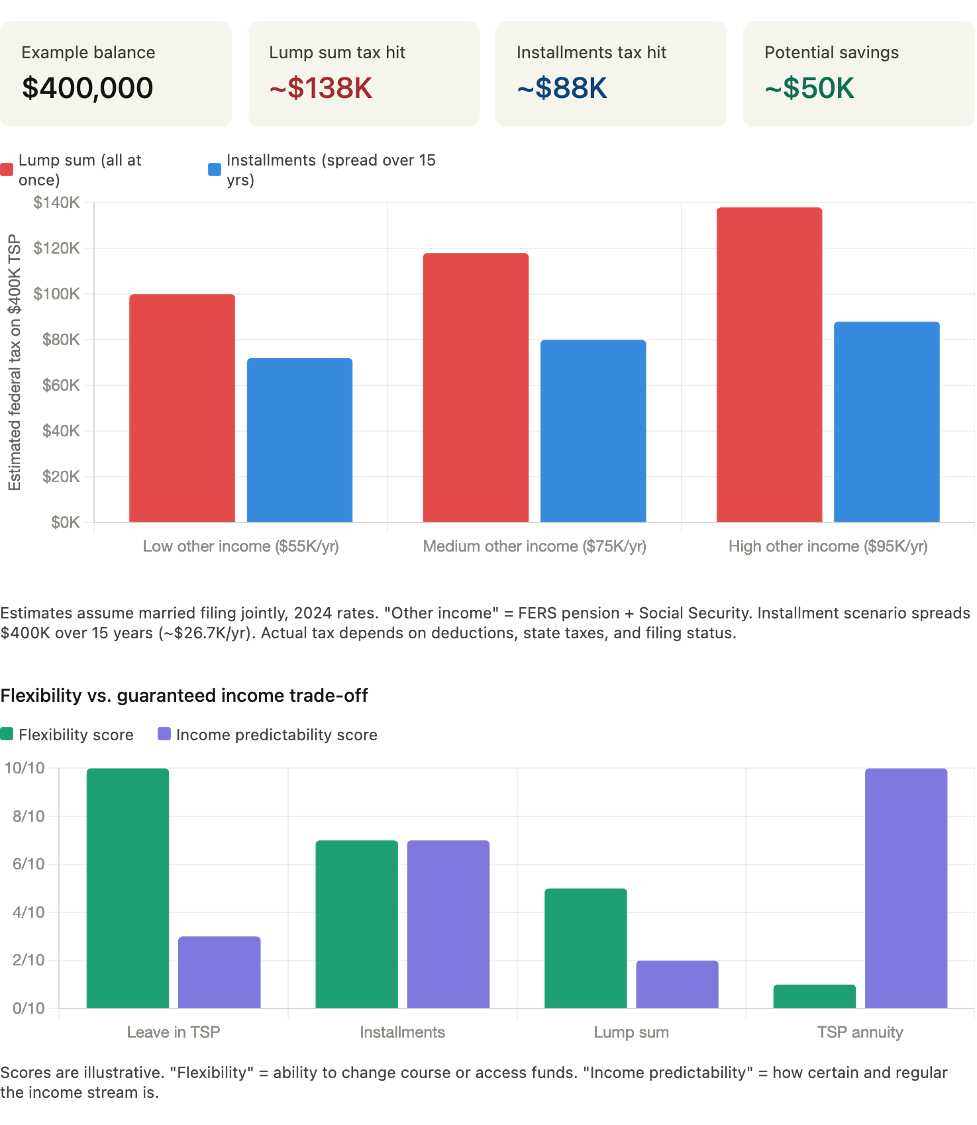

⚠️ The lump sum trap: Suppose you retire with a $400,000 traditional TSP balance and take it all at once. Added to your FERS annuity of $55,000 and Social Security of $20,000, your taxable income for that year is $475,000. You've just pushed a large portion of your money into the 35% federal bracket. A retiree who instead spread those withdrawals over 10–15 years might pay 22–24% on most of it. The difference on $400,000 can easily exceed $40,000–$50,000 in federal taxes alone.

Partial lump sums are different. Pulling $30,000 to pay off a car note or fund a home repair is a legitimate, targeted use. The problem is treating the lump sum as a default rather than a tool.

2. Monthly, Quarterly, or Annual Installments

You instruct TSP to send you regular payments on a schedule you define. There are two methods:

Fixed dollar amount: You choose how much — say, $2,500/month. TSP pays that amount until the account is depleted. If your balance grows or shrinks, the payments stay the same.

Life expectancy method: TSP divides your account balance by an IRS life expectancy factor each year and sends you that amount. As you age, the factor decreases, so your payments gradually increase (assuming your balance holds steady). The calculation is redone annually — you don't have to do anything.

Can you change the amount? You can change your fixed dollar amount once per calendar year, or switch to the life expectancy method. You can also switch from installments to other options, though switching to a TSP annuity is subject to restrictions.

Tax treatment: Each payment is ordinary income in the year received. This spreads your tax liability across many years — the core tax advantage of installments over a lump sum.

Who it suits: Retirees who want predictable, regular cash flow without locking up their money permanently. The life expectancy method is particularly well-suited if you want TSP to "do the math" on sustainable withdrawals.

3. TSP Life Annuity

You use some or all of your TSP balance to purchase a life annuity through MetLife, TSP's contracted annuity provider. In exchange for a lump sum of your savings, MetLife pays you a fixed monthly income for the rest of your life.

Options include:

- Single life annuity (payments stop at your death)

- Joint life annuity (continues to a survivor after your death — costs more)

- Inflation-indexed annuity (payments increase with CPI — costs more)

- Death benefit (returns remaining value to your estate — costs more)

Tax treatment: Monthly payments are ordinary income, just like installments.

Flexibility: None. This is the critical fact about TSP annuities: they are irreversible. Once MetLife has your money, you cannot undo the transaction, change your mind, or access the principal for an emergency. Your estate typically receives nothing unless you paid extra for a death benefit feature.

How the rate is set: MetLife prices the annuity based on the 10-year Treasury yield at the time of purchase. When interest rates are low, annuity payouts are lower — you get less income per dollar annuitized. This makes timing matter significantly.

Why most financial planners are skeptical: Most fee-only financial planners who specialize in federal retirement are lukewarm on TSP annuities for most retirees. The reasons: loss of all flexibility, no death benefit by default, rates that can be uncompetitive relative to what you'd earn keeping money invested, and the fact that FERS retirees already have a guaranteed income floor (FERS pension + Social Security + possibly the FERS Supplement). Adding a third guaranteed stream may not be worth the inflexibility.

When it might make sense: A retiree with little or no other guaranteed income, who has reason to believe they'll live a very long time, and who genuinely cannot self-manage investment withdrawals might benefit. It is a narrow use case.

4. Leave Money in TSP — The Underrated Option

You don't have to touch your TSP at retirement. You can leave it invested, continuing to grow, until you need it or are required to take distributions.

Why this is often the smart default:

- Expense ratios: TSP's index funds charge approximately 0.042% annually — among the lowest of any retirement vehicle in the world. A comparable S&P 500 index fund at a major brokerage typically charges 0.03%–0.20%. The TSP G Fund, available only to federal employees, offers Treasury-level returns with no principal risk — an option you simply cannot replicate outside TSP.

- No RMD pressure until 73: Under the SECURE 2.0 Act, Required Minimum Distributions don't begin until age 73. If you retire at 62, you have over a decade before TSP forces distributions.

- Partial withdrawals available: You can still take partial withdrawals from TSP as needed without committing to a full distribution strategy.

- Rollover flexibility: You can roll your TSP into an IRA at any time if you later decide you want more investment options.

Who it suits: Almost any retiree who has other income sources (FERS pension, Social Security, FERS Supplement) covering near-term expenses and who wants to preserve TSP's low costs and flexibility.

Comparison at a Glance

| Option | Flexibility | Tax Timing | Best For | Key Risk |

|---|---|---|---|---|

| Lump Sum | High before; none after | All in one year | Specific large purchase; IRA rollover | Large tax bill from bracket spike |

| Installments | Moderate; adjust annually | Spread over years | Steady income, tax efficiency | Must manage sustainability yourself |

| TSP Annuity | None — irreversible | Spread over lifetime | Longevity risk, no other guaranteed income | Locked in forever; no principal access |

| Leave in TSP | Highest | Deferred until withdrawal | Covering near-term needs with other income | RMDs begin at 73 regardless |

Rollover to IRA: When It Makes Sense

Rolling your TSP into a traditional or Roth IRA isn't one of TSP's four options — it's a separate action you can take alongside or instead of them. It makes sense when:

- You want more investment choices: TSP offers five core funds. An IRA at a major brokerage gives you access to thousands of ETFs, individual stocks, and bonds.

- Roth conversion planning: IRAs give you more flexibility to execute multi-year Roth conversion strategies.

- Estate planning: IRAs offer more options for beneficiary designations and inherited account rules.

The trade-off: You'll almost certainly pay higher expense ratios than TSP's ~0.042%. And you permanently give up the G Fund. These aren't reasons to never roll over, but they're costs worth quantifying before you do.

The RMD Clock

At age 73, Required Minimum Distributions kick in — TSP and the IRS will require you to take out a minimum amount annually, whether you need the money or not, based on your account balance and IRS life expectancy tables.

Important Roth distinction: Roth TSP accounts are no longer subject to RMDs during the owner's lifetime as of 2024 (a SECURE 2.0 change). Roth IRAs also have no RMDs for the original owner. Traditional TSP and traditional IRAs are both subject to the age-73 requirement.

If you expect to have a large TSP balance at 73, planning ahead — through Roth conversions or structured early withdrawals — can reduce your eventual RMD burden and the tax hit that comes with it.

A Note on the Age 55 Rule

Federal employees who separate from service at age 55 or older can take TSP withdrawals without the 10% early withdrawal penalty. This is different from the IRA rule, which requires age 59½ for penalty-free withdrawals. If you retire at 57, for example, you can access your TSP freely — but moving those funds to an IRA would subject them to IRA rules, potentially creating a penalty window if you're under 59½.

Three Questions Before You Decide

Before selecting a withdrawal strategy, work through these:

-

Do I have enough guaranteed income to cover essential expenses? If your FERS pension, Social Security, and FERS Supplement (if applicable) already cover your fixed costs, TSP can serve as flexible, supplemental income — which favors leaving it alone or using installments rather than annuitizing.

-

What is my tax situation in the first few years of retirement? If you retire at 60 and delay Social Security until 67, your early retirement years may be your lowest-income years ever — a prime window for strategic Roth conversions or larger withdrawals at low tax rates.

-

What do I actually need the money for? A specific goal (mortgage payoff, lump sum gift) favors a targeted partial withdrawal. Ongoing living expenses favor installments. Longevity anxiety might favor a partial annuity. Preservation and flexibility favor leaving it in TSP.