The 4% rule is the most cited piece of retirement planning advice in personal finance. Withdraw 4% of your portfolio per year, adjust for inflation, and your money has a high probability of lasting 30 years. It is a reasonable starting point for most retirees.

It was not built for federal employees with a FERS pension.

That is not a criticism of the rule — it is a statement about the assumptions behind it. The research that produced the 4% guideline assumed a retiree whose entire income in retirement comes from an investment portfolio. When you layer a guaranteed pension on top of a TSP account, the math changes in ways that most federal employees do not fully account for.

Why the pension changes everything

Think of your FERS annuity as a bond. It pays a fixed monthly amount for the rest of your life, with a modest inflation adjustment (COLA) each January. In a traditional investment portfolio, the bond allocation provides stability — it reduces sequence-of-returns risk and provides income during market downturns so you do not have to sell equities at a loss.

Your pension does exactly this job, and it does it more reliably than any bond fund because it carries no default risk and no duration risk. It just pays, every month, regardless of what the stock market does.

This has two practical implications for how you should think about your TSP.

First, your TSP can afford to be more aggressively allocated. If your pension covers your essential expenses — housing, food, healthcare — your TSP withdrawals are funding discretionary spending. You are not drawing on the TSP to survive during a market downturn. You can afford to keep a higher equity allocation (more C Fund, less G Fund) because a bad sequence of returns does not threaten your ability to pay your bills.

Second, your safe withdrawal rate from the TSP is higher than 4%. The 4% rule is calibrated to sustain a portfolio with no other income through 30 years of withdrawals. When a pension covers your base expenses, the TSP is a supplemental income stream, not your only income. A 4.5% or even 5% withdrawal rate from the TSP may be entirely appropriate, depending on how much the pension covers.

The right framework: calculate your income gap first

Before you can set a TSP withdrawal rate, you need to know what job the TSP actually needs to do. This is a three-step process.

Step 1: Establish your target monthly spending.

Be honest and specific. What does a comfortable retirement look like for you? Include housing (even if the mortgage is paid off, there are taxes and maintenance), healthcare premiums and out-of-pocket costs, transportation, food, travel, and discretionary spending. Most financial planners use 70–85% of pre-retirement income as a starting point, but this is highly personal.

Step 2: Calculate your guaranteed income floor.

Add up every guaranteed income source:

- FERS annuity (monthly pension amount after any MRA+10 reduction)

- FERS Supplement, if applicable (until age 62)

- Social Security, once you claim it

- Any spouse pension or Social Security

This is income that arrives regardless of market conditions. It is your floor.

Step 3: Find the gap.

Monthly gap = Target spending − Guaranteed income floor

This gap is what your TSP needs to cover. Your withdrawal rate calculation applies to the gap, not to your total retirement spending.

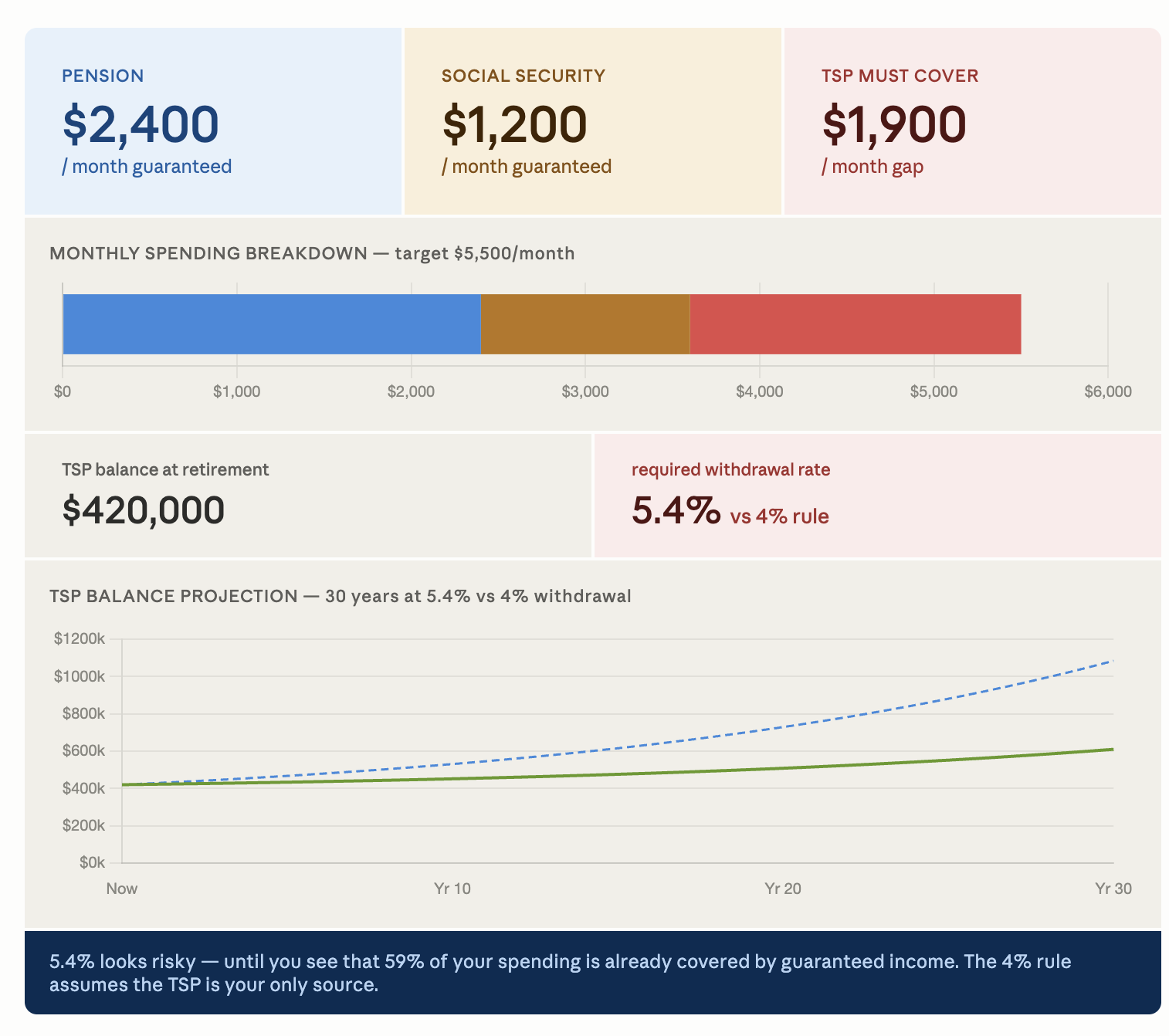

Worked example

A FERS employee retires at 62 with a pension of $2,400/month and Social Security of $1,200/month. Their target monthly spending is $5,500/month. The gap is $1,900/month — or $22,800/year.

If their TSP balance at retirement is $420,000, the withdrawal rate needed to cover the gap is:

$22,800 ÷ $420,000 = 5.4%

Under the strict 4% rule, this looks alarming. But the context matters: the $22,800 annual withdrawal represents only 41% of their total retirement spending. The other 59% is covered by guaranteed income that will never run out. The sequence-of-returns risk that the 4% rule is designed to protect against is dramatically reduced when most of your income is guaranteed.

Whether 5.4% is sustainable in this scenario depends on age, TSP allocation, and spending flexibility. But it is not inherently reckless — and treating it as equivalent to a 5.4% withdrawal from a portfolio that must cover all expenses would lead you to significantly over-save at the cost of working longer than necessary.

The two-phase problem: before and after 62

For FERS employees who retire before 62, the income picture is not static. It changes at two points:

- At retirement: FERS pension begins, FERS Supplement begins (if eligible)

- At age 62: FERS Supplement stops, Social Security can begin

This means you have two distinct phases with different income gaps, and your TSP strategy should account for both.

Phase 1 (retirement to 62): Your income includes the pension plus the supplement. The gap may be smaller than you expect if the supplement is meaningful — $800 to $1,200/month is common for mid-career federal employees.

Phase 2 (62 onward): The supplement stops. If you have not yet claimed Social Security, your guaranteed income floor drops. This is the moment when TSP withdrawals may need to increase — temporarily, until Social Security begins.

The cleanest approach is to model both phases separately. What is the gap in Phase 1? What is the gap in Phase 2 before Social Security? What is the gap after Social Security begins? These may be three different numbers requiring three different withdrawal rates from the TSP.

What this means for your TSP allocation

The pension's presence as a guaranteed income floor allows a more aggressive TSP allocation than a typical retiree should hold. However, "more aggressive" is not unlimited.

A reasonable framework based on your pension coverage ratio — the fraction of your essential expenses covered by guaranteed income:

| Pension covers | Suggested TSP equity allocation |

|---|---|

| Less than 50% of expenses | 50–60% equities |

| 50–70% of expenses | 60–70% equities |

| 70–90% of expenses | 70–80% equities |

| More than 90% of expenses | 80%+ equities (if comfortable) |

If your pension and Social Security together cover all your essential expenses and your TSP is purely discretionary income, you could in theory hold 100% equities in your TSP. Whether you want that level of volatility is a personal question. But the traditional argument for shifting heavily to bonds in retirement — protecting against sequence-of-returns risk — applies much less when a pension provides that protection instead.

Required Minimum Distributions — the tax surprise

One aspect of TSP withdrawals that catches federal retirees off guard is the Required Minimum Distribution (RMD) at age 73.

If you have a substantial TSP balance — $500,000 or more — and a pension that already covers most of your expenses, your RMDs may be larger than you want or need. The IRS requires you to withdraw a minimum each year regardless of whether you need the income. These withdrawals are taxable, and they can push you into a higher bracket when combined with pension income and Social Security.

The window between retirement and age 73 (or age 70 if you want to delay RMDs as long as possible) is an opportunity for Roth conversion. Moving money from your Traditional TSP to a Roth IRA in years when your income is lower can reduce future RMDs and future tax liability. This is a complex planning question that depends heavily on your individual tax situation and is worth discussing with a tax professional.

The contribution rate decision in the years before retirement

None of the withdrawal strategy thinking above matters if you arrive at retirement without enough TSP balance to cover your gap.

The single most impactful decision most federal employees can make in the 5–10 years before retirement is to increase their TSP contribution rate. The math on this is striking: going from 5% to 10% of salary with 10 years left adds far more to your balance than the same dollar amount invested earlier, because the compounding period is shorter but the absolute amount is larger and the pre-retirement tax deduction is at your peak earning years.

If you are more than 5 years from retirement and your TSP contribution is below 10%, that is almost certainly the highest-return financial decision available to you — higher than paying down a low-interest mortgage, higher than taxable investment accounts for most employees.

The contribution limit for 2025 is $23,500, plus a $7,500 catch-up contribution if you are age 50 or older. Maximising the catch-up in the final years before retirement, if cash flow allows, is worth serious consideration.

The question to ask yourself

The most useful reframe for federal employees thinking about TSP withdrawal strategy is this: what is the TSP actually for?

For some employees, the pension is generous enough that the TSP is a discretionary fund — travel money, home improvement, gifts to family. A higher withdrawal rate and a more aggressive allocation make sense.

For others, the pension alone does not come close to covering their target lifestyle, and the TSP is doing heavy lifting as a primary income source. A lower withdrawal rate and a more conservative allocation are appropriate.

The answer is not universal. It depends on your specific pension amount, your Social Security timing, your spending target, and your comfort with volatility. What is universal is that the standard 4% rule — designed for portfolios carrying the full burden of retirement income — is not the right starting point for a federal employee with a guaranteed annuity.

Model your gap first. Then choose your withdrawal rate.