One of the most valuable and least understood benefits in FERS is the Special Retirement Supplement — often called the FERS Supplement or SRS. For federal employees who retire before age 62 under an immediate full retirement, it provides hundreds of dollars per month in additional income until Social Security can begin.

What is the FERS Supplement?

The FERS Supplement is a monthly payment from OPM designed to approximate the Social Security benefit you earned during your federal career. It exists because Social Security cannot be claimed before age 62, but FERS employees can retire as early as their Minimum Retirement Age — which for most current employees is 56 or 57.

Without the supplement, a FERS employee retiring at 57 would have a multi-year income gap between their pension and the start of Social Security. The supplement fills that gap.

Who qualifies?

You receive the FERS Supplement if you retire under immediate full retirement before age 62:

- MRA + 30 years of service → qualifies

- Age 60 + 20 years of service → qualifies

- Age 62 or older → does not receive supplement (Social Security can begin directly)

- MRA + 10 (reduced retirement) → does not qualify

- Deferred retirement (claim at 62 after separating early) → does not qualify

The common thread is immediate unreduced retirement. If your pension was reduced for any reason, or if you're deferring your claim, the supplement does not apply.

How is the supplement calculated?

OPM uses this formula:

Annual Supplement = (Estimated SS benefit at 62) × (Years of FERS service ÷ 40)

In plain terms: take the Social Security benefit you would receive at 62, multiply it by the fraction of a full 40-year career you spent in federal service.

Worked example

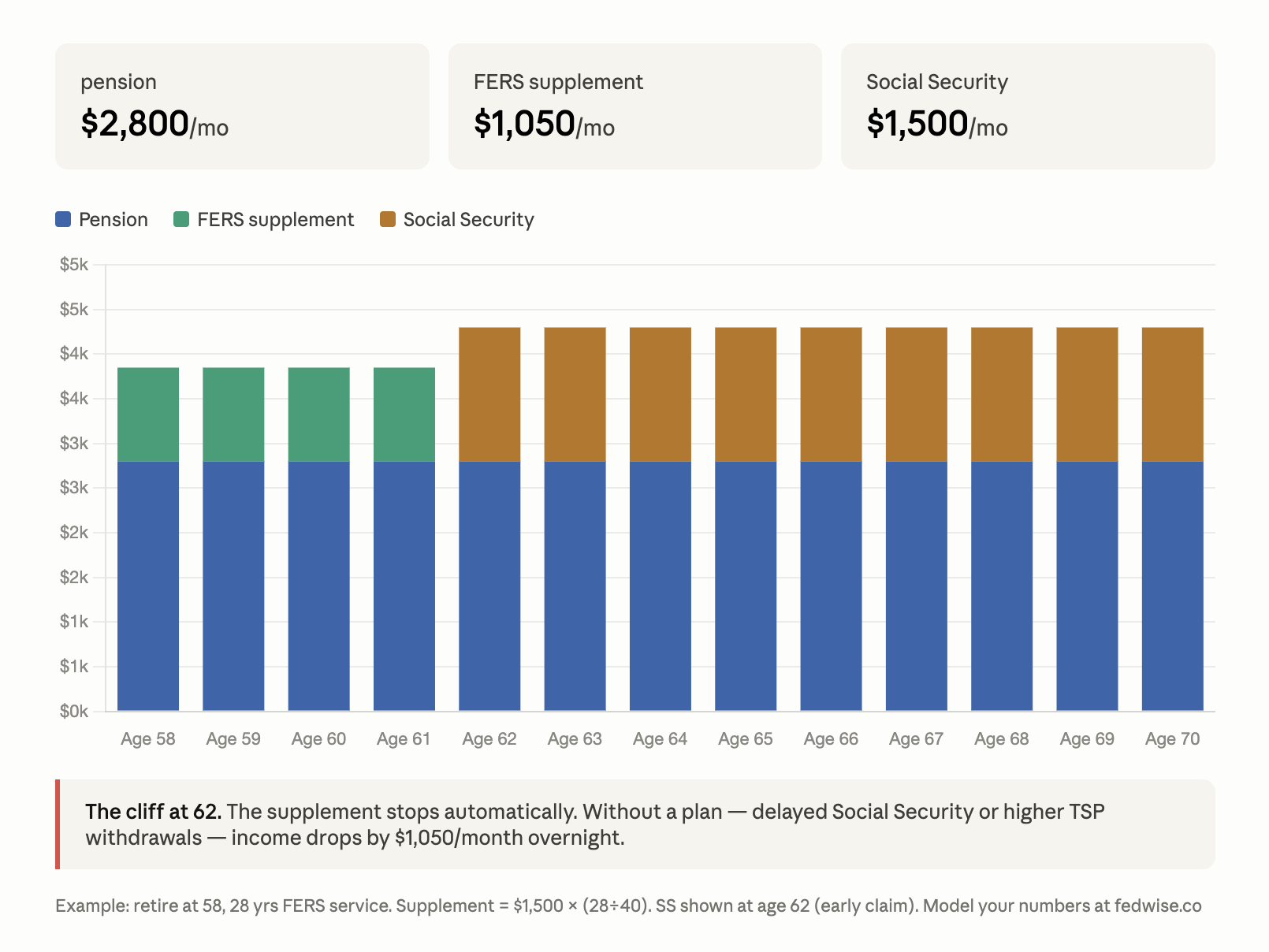

- Employee retires at 58 with 28 years of FERS service

- Estimated Social Security benefit at 62: $18,000/year ($1,500/month)

- Supplement = $18,000 × (28 ÷ 40) = $12,600/year = $1,050/month

That $1,050/month supplement continues every month from retirement until the employee's 62nd birthday, at which point it stops automatically and actual Social Security can begin.

How does OPM estimate your Social Security benefit?

OPM uses your reported federal earnings to estimate what your Social Security would be at 62. This is an approximation — it uses your federal salary history without access to your complete Social Security earnings record (which may include pre-federal or private sector work).

If you worked in the private sector before federal service, your actual Social Security benefit is likely higher than OPM estimates, because your private sector earnings add to your AIME calculation. The supplement OPM pays is based only on your federal service fraction.

Always check your official Social Security estimate at ssa.gov/myaccount. The difference between OPM's estimate and your actual SS benefit can be significant.

The earnings test

If you continue working after retirement — part-time, consulting, or any earned income — your FERS Supplement is subject to the Social Security earnings test.

For 2025, the exempt amount is approximately $22,320 per year. For every $2 you earn above this threshold, your supplement is reduced by $1.

Example: You earn $30,000 in part-time income after retirement. That's $7,680 above the exempt amount. Your annual supplement is reduced by $3,840 ($320/month).

Important: the earnings test applies only to earned income — wages and self-employment. Investment income, pension income, and TSP withdrawals do not count toward the test.

When does it stop?

The supplement stops automatically the month you turn 62 — no action required. OPM ceases payment and you become eligible to begin Social Security. You are not required to claim Social Security at 62; you can delay to 67 for full benefit or 70 for maximum benefit. But the supplement ends regardless of your Social Security claiming decision.

Planning around the supplement

Factor it into your cash flow projections. The supplement can represent $800–$1,400/month for mid-career federal employees. Your retirement plan should account for the income drop at 62 and replace it with either Social Security or increased TSP withdrawals.

Protect your FEHB eligibility. The supplement is only available to employees who retire under immediate full retirement — the same retirement that qualifies you to carry FEHB into retirement (the 5-year rule). If you qualify for the supplement, you almost certainly qualify to keep your health insurance. These benefits travel together.

Don't count on MRA+10 qualifying. This is the most common misconception. MRA+10 gives you access to immediate retirement — but it's a reduced retirement, and the supplement is not paid. If having the supplement matters to you, the options are to reach 30 years of service before your MRA, or wait until age 60 with 20 years.