Most federal employees think of the G Fund as "the safe option." That framing is not wrong — it just undersells what the G Fund actually is, and badly obscures what it costs you.

The G Fund is one of the most structurally unusual investments available to any American worker. Understanding exactly what it is — not just that it is "safe" — is the first step to using it correctly.

What the G Fund Actually Is

The Government Securities Investment Fund invests in special-issue U.S. Treasury securities created exclusively for the TSP. These are not bonds you can buy on the open market. They are non-marketable instruments that exist solely inside the federal retirement system.

Here is the structural advantage that makes the G Fund unlike anything in the private sector: it earns a long-term interest rate on a short-term instrument. The interest rate is recalculated monthly and set to the weighted average yield of all outstanding Treasury notes and bonds with four or more years to maturity. But unlike an actual long-term Treasury bond, the G Fund's principal cannot decline. Market rates can move in any direction — your G Fund balance will never fall.

That combination — long-term yield with zero principal risk — does not exist anywhere else. No money market fund, no stable value fund, no savings account offers it. It is a structural benefit exclusive to TSP participants.

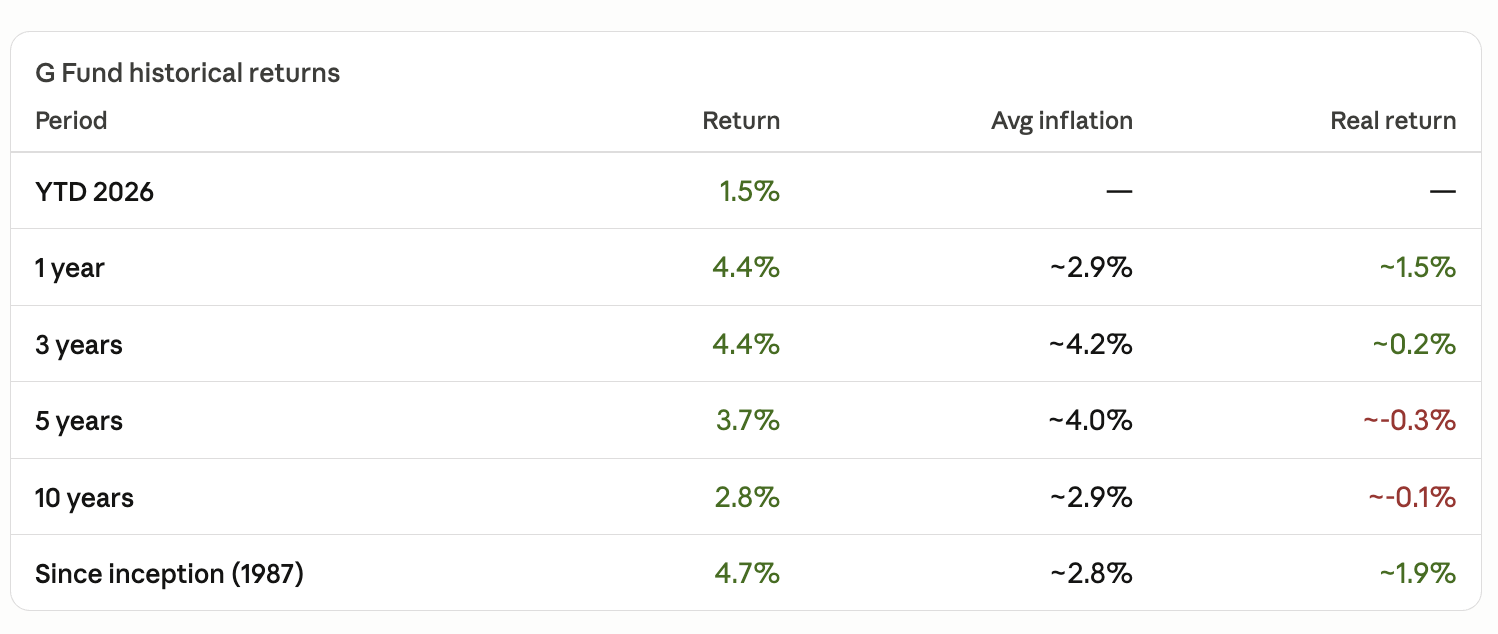

Since its inception in April 1987, the G Fund has produced a compound annualized return of approximately 4.7%. Interest is credited daily and compounds monthly. The TSP expense ratio across all funds runs about 0.042% — compared to 0.5–1.5% for comparable stable value funds in private-sector 401(k) plans. That cost advantage alone is meaningful over a career.

Where the G Fund Shines

Used deliberately, the G Fund is an excellent tool.

Near-term spending. Money you will need within 6–24 months — an emergency reserve, a planned purchase, a buffer against early retirement sequence risk — belongs somewhere it cannot drop. The G Fund is ideal.

Sequence-of-returns protection. The most dangerous years for a retirement portfolio are the first two to five years of withdrawals. A sharp market decline early in retirement, combined with ongoing withdrawals, can permanently impair a portfolio's longevity. Keeping one to two years of expenses in the G Fund lets you draw from a stable source while equities recover.

Rebalancing anchor. When the C, S, or I Fund drops significantly, the G Fund is what you sell to buy those funds at lower prices. A disciplined rebalancing strategy actually converts G Fund stability into equity gains over time.

Pre-retirement glide path. If you are within two to three years of retirement, gradually shifting a portion of your TSP into G reduces your exposure to a poorly timed market decline just before you need the money.

The Hidden Cost — and the Real Numbers

Here is where the framing in the G Fund's name becomes dangerous. "Safe" refers to nominal principal. It says nothing about purchasing power.

Inflation has averaged roughly 3% annually over long periods. The G Fund's current annualized return is approximately 4.4%. That leaves a real (inflation-adjusted) return of about 1.4% — and in periods when inflation has run higher, the real return has been near zero or negative. Your account balance grows. What that balance buys does not keep pace.

The opportunity cost against equities is more dramatic. Consider two hypothetical paths for $100,000:

| G Fund (~4.4%) | C Fund (historical ~10.4%) | |

|---|---|---|

| Year 10 | $153,000 | $269,000 |

| Year 20 | $235,000 | $723,000 |

| Year 30 | $360,000 | $1,943,000 |

Illustrative projections. Not a guarantee of future performance.

At 20 years, the gap is nearly $490,000 on a single $100,000 investment. For a federal employee in their 30s or 40s with a significant G Fund allocation, the compounding drag is not a rounding error — it is the difference between a comfortable retirement and a constrained one.

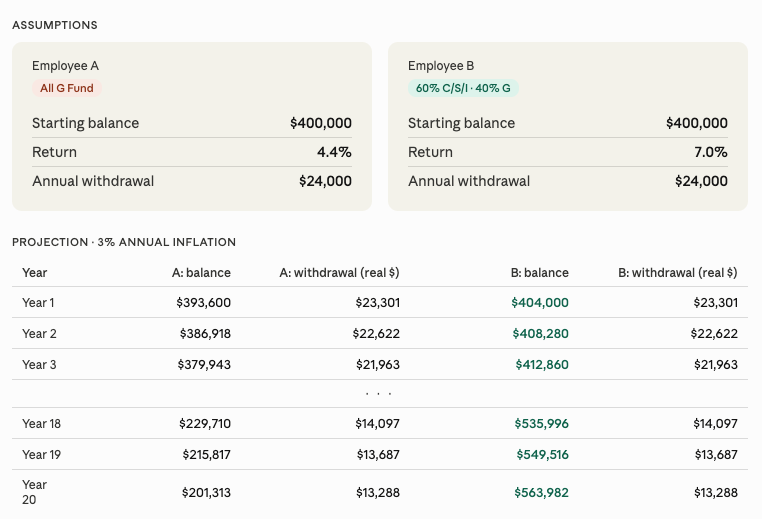

A Worked Example: Two FERS Employees at Retirement

Both employees are FERS, both retire at 62 with 30 years of service, and both have accumulated $400,000 in their TSP. The difference is how they invested it.

Employee A — All G Fund

- TSP balance at retirement: $400,000

- G Fund return: ~4.4%

- Annual withdrawal: $24,000 (~6% of balance)

- Inflation: 3%

In Year 1, the account earns roughly $17,600 in interest. After the $24,000 withdrawal, the balance falls by approximately $6,400. Each subsequent year, that same $24,000 withdrawal purchases less in real terms while the account slowly shrinks. By Year 20, the purchasing power of the annual withdrawal has eroded to the equivalent of about $13,300 in today's dollars — and the account may be approaching depletion.

Employee B — Balanced (60% C/S/I, 40% G Fund)

- TSP balance at retirement: $400,000

- Blended return assumption: ~7% (historical average for a diversified equity/bond mix)

- Annual withdrawal: $24,000

- Inflation: 3%

The equity portion grows faster than withdrawals in most years. The G Fund serves as a near-term cash buffer, funding one to two years of withdrawals without forcing equity sales during downturns. The portfolio sustains 30-plus years with a high probability of leaving a meaningful residual balance.

These are illustrative projections, not guaranteed outcomes. Individual results will vary based on actual market returns, withdrawal timing, and other factors.

The difference is not about risk tolerance in the abstract. It is about understanding which risks are actually present in each strategy. Employee A faces near-certain purchasing-power erosion and meaningful depletion risk. Employee B faces market volatility — but with the buffer to absorb it.

Five Mistakes That Cost Federal Employees the Most

1. Treating G Fund as the default rather than a deliberate choice. Many employees — especially those who joined federal service before automatic enrollment steered new hires into L Funds — are sitting in 100% G Fund because they never changed their initial election. That is not a strategy. It is inertia with a compounding penalty.

2. Panic-shifting to G during market downturns. During the tariff-driven market selloff of March–April 2025, approximately $33 billion moved into the G Fund while roughly $29 billion left the C, S, and I Funds. Most of that money moved at or near the bottom and missed the subsequent recovery. Locking in losses by fleeing to safety after the drop is one of the most reliable ways to permanently impair a retirement account.

3. Rolling TSP to an IRA and losing G Fund access entirely. No private-sector fund replicates what the G Fund does. Once you roll your TSP to an IRA, you lose access to this instrument permanently. If preserving G Fund access matters to your strategy — and for most retirees, it should — staying in TSP is the only way to keep it.

4. Confusing "no principal loss" with "no risk." The G Fund eliminates one specific risk: nominal principal loss from rate movements. It does not eliminate inflation risk, longevity risk, or sequence-of-returns risk if G Fund is your only holding. Those risks are quieter, but they are real — and for a retirement that may span 25–30 years, they are arguably more consequential.

5. Over-weighting G in accumulation years, under-weighting in early retirement. This is the reverse of optimal. When you are 35 and have three decades before you need the money, you can ride out market cycles — heavy equity exposure is appropriate. When you are 63 and taking withdrawals, a significant G Fund buffer reduces sequence risk in the years that matter most. Many employees do the opposite: they are heavily in equities late in their career because they never revisited their allocation, then panic into G after the first market drop in retirement.

The Right Frame

The G Fund is not the default. It is a precision instrument — one of the best risk-management tools available to any American investor, deployed strategically in the right size, at the right time, for the right purpose.

Used that way, it is genuinely exceptional. Used as a passive holding for an entire career, it is a slow, quiet drag on everything compounding could have built.