The 25x Rule Was Not Built for You

If you've ever typed "how much do I need to retire" into a search engine, you've seen the 25x rule: multiply your annual expenses by 25, and that's your number. For a $80,000 lifestyle, that's $2 million.

That number is correct — for someone whose portfolio has to do all the heavy lifting. It assumes zero pension income, zero Social Security (or at least ignores it), and a portfolio generating 100% of retirement cash flow at a 4% withdrawal rate.

That is not you.

As a FERS employee, you have a guaranteed pension. Every dollar of that pension is a dollar your TSP does not have to produce. And the math cuts sharply in your favor: each $1,000/month in pension income reduces your required TSP balance by $300,000 at a 4% withdrawal rate.

Read that again. A $3,000/month pension means you need $900,000 less in your TSP than someone with no pension targeting the same lifestyle.

The right question isn't "how much TSP do I need to fund my whole retirement?" It's "how much TSP do I need to cover the gap my pension and Social Security don't fill?"

The Correct Framework: Calculate Your Gap

Here is the four-step process:

Step 1: Set your target monthly income. A common benchmark is 80% of your current salary. At $90,000, that's $72,000/year, or $6,000/month.

Step 2: Add up your guaranteed income floor. This includes your FERS pension, Social Security (at the age you plan to claim it), and — if you retire before 62 — the FERS Supplement.

Step 3: Subtract the floor from your target. That's your TSP gap. This is the monthly amount your TSP withdrawals need to cover.

Step 4: Multiply the annual gap by 25 (for a 4% withdrawal rate) or 20 (for 5%). This is your TSP target — not your total spending target.

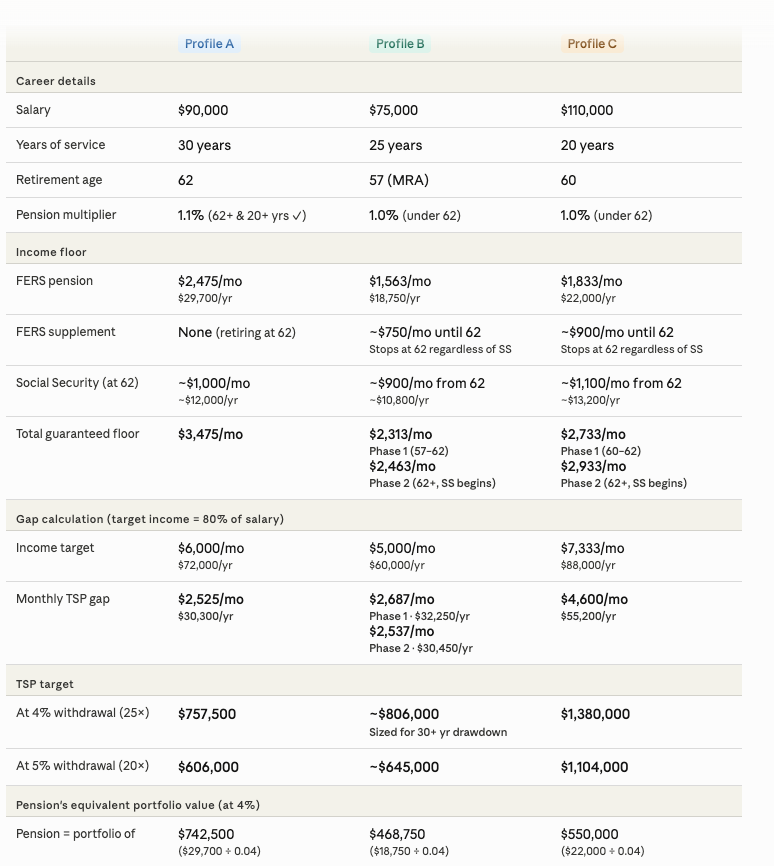

Three Profiles, Three Very Different Numbers

Profile A: 30 Years, $90k Salary, Retiring at 62

This is the straightforward case — long career, retiring right at the age when SS kicks in and the enhanced pension multiplier applies.

| Monthly | Annual | |

|---|---|---|

| Target income (80% of $90k) | $6,000 | $72,000 |

| FERS pension (High-3 × 30 yrs × 1.1%) | $2,475 | $29,700 |

| Social Security at 62 | ~$1,000 | ~$12,000 |

| Guaranteed floor | $3,475 | $41,700 |

| TSP gap | $2,525 | $30,300 |

TSP target at 4% withdrawal: $757,500 TSP target at 5% withdrawal: $606,000

Note: the 1.1% multiplier applies here because this employee is both 62+ and has 20+ years of service — both conditions must be met.

Profile B: 25 Years, $75k Salary, Retiring at 57 (MRA)

Early retirement creates two distinct phases because the FERS Supplement ends at 62, regardless of when you claim Social Security. This is the "supplement cliff" — a real income shift you have to plan for.

Phase 1: Ages 57–62 (with FERS Supplement)

The FERS Supplement approximates the Social Security benefit earned during federal service. For this profile, estimate roughly $700–$800/month.

| Monthly | Annual | |

|---|---|---|

| Target income (80% of $75k) | $5,000 | $60,000 |

| FERS pension (High-3 × 25 yrs × 1.0%) | $1,563 | $18,750 |

| FERS Supplement (estimated) | $750 | $9,000 |

| Guaranteed floor | $2,313 | $27,750 |

| TSP gap (Phase 1) | $2,687 | $32,250 |

Phase 2: Ages 62+ (Supplement ends, SS begins)

| Monthly | Annual | |

|---|---|---|

| Target income | $5,000 | $60,000 |

| FERS pension | $1,563 | $18,750 |

| Social Security at 62 | ~$900 | ~$10,800 |

| Guaranteed floor | $2,463 | $29,550 |

| TSP gap (Phase 2) | $2,537 | $30,450 |

In this case, the gaps are similar, but Phase 1 lasts five years. Your TSP target needs to be sized for the longer drawdown period of early retirement (potentially 30+ years), which pushes the multiplier toward 25x or slightly above.

TSP target at 4% withdrawal: ~$806,000 (sized for Phase 2 gap, with buffer for 30+ year drawdown)

Profile C: 20 Years, $110k Salary, Retiring at 60

Higher salary, but a shorter career and retirement at 60 means the 1.1% enhanced multiplier does not apply — that requires age 62+ and 20+ years. At 60, the standard 1.0% multiplier is used.

| Monthly | Annual | |

|---|---|---|

| Target income (80% of $110k) | $7,333 | $88,000 |

| FERS pension (High-3 × 20 yrs × 1.0%) | $1,833 | $22,000 |

| FERS Supplement (est., until 62) | ~$900 | ~$10,800 |

| Guaranteed floor (pre-62) | $2,733 | $32,800 |

| TSP gap | $4,600 | $55,200 |

TSP target at 4% withdrawal: $1,380,000

The higher salary and the income target drive this number up significantly. If this employee waited until 62, the pension would jump to 1.1% × 20 years × High-3, adding roughly $2,400/year to guaranteed income — and cutting the TSP target by around $60,000.

Your Pension Has a Hidden Portfolio Value

Here's a reframe that changes how most federal employees see their retirement picture.

A 4% withdrawal rate means every $25 of portfolio generates $1/year. Flip that around: every $1/year of guaranteed income is equivalent to having $25 in your portfolio.

A $30,000/year pension is worth the same as a $750,000 investment portfolio in terms of retirement income it produces. Many federal employees — especially those who didn't start investing early — are far wealthier in retirement terms than their TSP balance suggests.

You may already be a "pension millionaire" without knowing it.

How Retirement Age Changes Everything

Retiring earlier means your TSP has to last longer and cover more years before Social Security bridges the gap. Retiring later increases both your pension (more service years, higher High-3) and shrinks the TSP drawdown period.

| Retirement Age | Pension Multiplier | SS Availability | TSP Drawdown Period (to 90) |

|---|---|---|---|

| 57 (MRA) | 1.0% | Not yet | ~33 years |

| 60 | 1.0% | Not yet | ~30 years |

| 62 | 1.0% or 1.1%* | Available | ~28 years |

| 65 | 1.1%* | Available + Medicare | ~25 years |

*1.1% requires 62+ AND 20+ years of service

Working even one or two additional years often delivers a disproportionate benefit: higher pension, shorter drawdown, and potentially a higher High-3 average.

If You're Behind — You Probably Need Less Than You Think

The pension changes the math in your favor. Before panicking about a TSP balance that looks short of $1 million, run your actual gap calculation. Most federal employees will find their target is meaningfully lower than generic retirement calculators suggest.

That said, if you do want to accelerate:

- Catch-up contributions after 50 allow an additional $7,500/year (2026 limit) — that's an extra $37,500 over five years before retirement, plus growth.

- Working one additional year at peak salary typically raises your High-3, adds a service year to the pension formula, and lets your TSP grow — a triple compounding effect.

- Adjusting your spending target from 80% to 75% of salary can cut your TSP target by $150,000–$200,000 for a mid-career employee.

Ballpark TSP Target Table

Estimates only. Assumes 80% income target, 4% withdrawal rate, SS of ~$12,000/yr at 62, and High-3 equal to final salary. Individual results will vary based on actual High-3, SS history, and spending.

| Salary | Years of Service | Retire at 57 | Retire at 60 | Retire at 62 |

|---|---|---|---|---|

| $60,000 | 20 years | ~$725,000 | ~$650,000 | ~$500,000 |

| $75,000 | 25 years | ~$825,000 | ~$750,000 | ~$575,000 |

| $90,000 | 30 years | ~$950,000 | ~$875,000 | ~$750,000 |

| $110,000 | 20 years | ~$1,450,000 | ~$1,380,000 | ~$1,150,000 |

| $110,000 | 30 years | ~$1,000,000 | ~$925,000 | ~$775,000 |

The takeaway: years of service matter enormously. A $110k employee with 30 years of service needs significantly less TSP than the same employee with 20 years — because the pension does much more of the work.